Introduction

Life is unpredictable — job loss, medical emergencies, car repairs, or unexpected bills can strike when you least expect it. That’s where an emergency fund comes in. It’s a financial safety net that provides peace of mind and protection when things don’t go as planned. But how much should you save? This guide will help you determine the right amount and how to start building it.

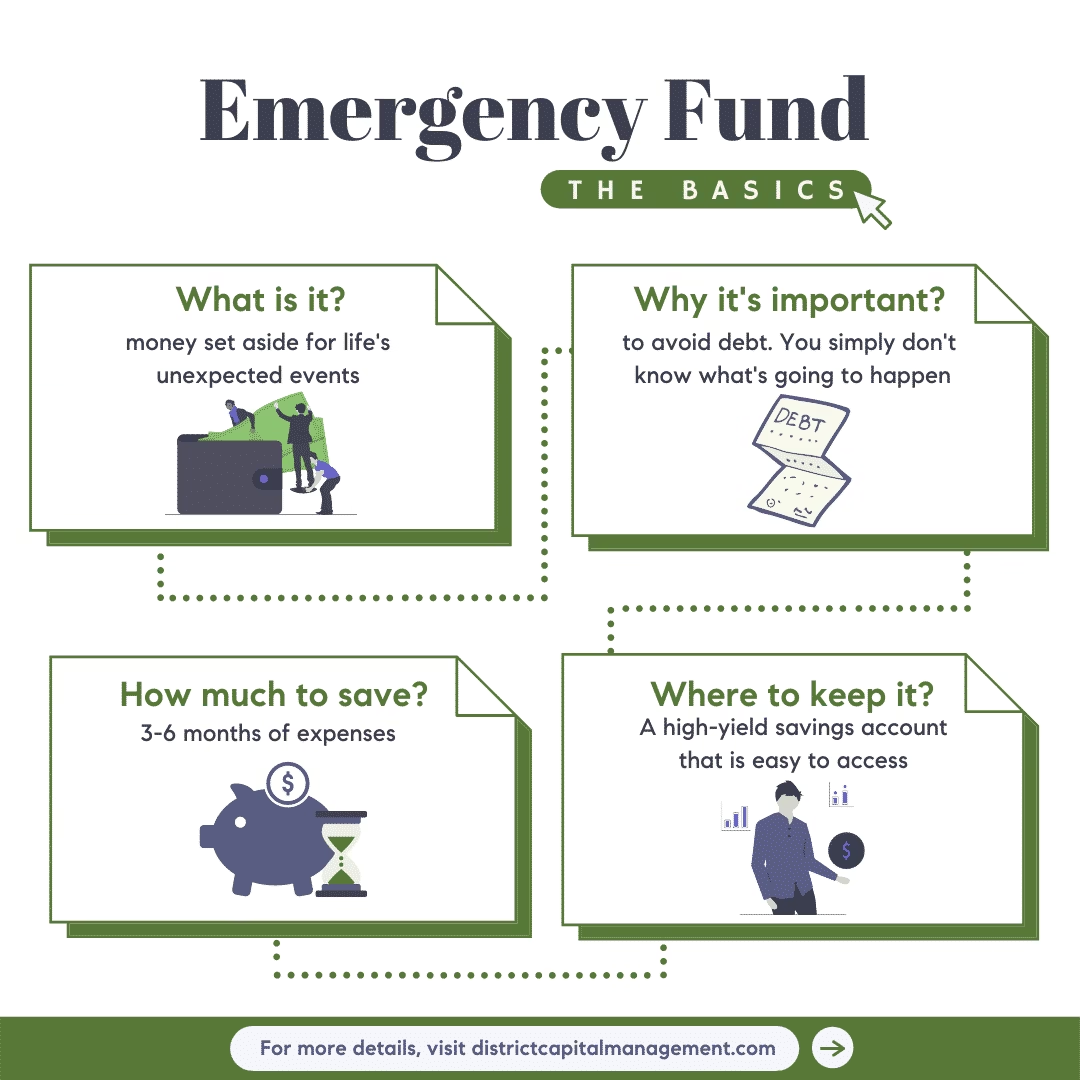

1. What Is an Emergency Fund?

An emergency fund is money set aside specifically for unexpected expenses. It’s not for vacations or new gadgets — it’s for true emergencies that can disrupt your financial stability.

Common uses include:

- Medical emergencies

- Job loss or income reduction

- Major car or home repairs

- Unexpected travel or family crises

2. Why It Matters

- Avoid debt: A solid fund helps you avoid credit cards or loans during a crisis.

- Reduce stress: Knowing you’re financially prepared brings peace of mind.

- Stay on track: It protects your budget, savings goals, and long-term plans.

3. How Much Is Enough?

There’s no one-size-fits-all number, but here are general guidelines:

- Starter Goal: ₹25,000 to ₹50,000 for basic emergencies (especially if you’re just beginning).

- Standard Rule: 3 to 6 months’ worth of living expenses.

- Consider your situation:

- Stable job & low expenses: 3 months may be enough.

- Freelance/irregular income: Aim for 6–12 months.

- Dependents or high-risk job: Lean toward the higher end.

- Stable job & low expenses: 3 months may be enough.

To calculate:

Add up your essential monthly expenses:

Rent + utilities + groceries + insurance + transportation = monthly need.

Multiply by 3–6 based on your situation.

4. Where to Keep Your Emergency Fund

- High-yield savings account: Safe, accessible, and earns interest.

- Money market account: Slightly higher interest, still liquid.

- Avoid keeping it in investment accounts where funds may fluctuate or be hard to withdraw quickly.

5. How to Start Saving

- Set a monthly goal: Even ₹1,000–₹2,000/month adds up.

- Automate it: Set up automatic transfers to a separate savings account.

- Cut back on extras: Reduce dining out, subscriptions, or impulse buys.

- Use windfalls: Tax refunds, bonuses, or gifts can give your fund a boost.

6. When to Use (and Not Use) It

Use it when:

- There’s a true, unforeseen emergency.

- Your basic needs are at risk.

Don’t use it for:

- Planned purchases

- Vacations

- Minor inconveniences

Conclusion

An emergency fund is one of the smartest financial moves you can make. It acts as your financial shield, protecting you from debt and anxiety when life throws curveballs. Start small if needed — the important part is starting. Future-you will be grateful.